In the U.S., stories of four- and five-digit hospital bills facing the uninsured and underinsured abound. It is well known that many Americans lack adequate health insurance coverage; prior to the passage of the Affordable Care Act in 2010, 18.2 percent of Americans were uninsured. Even following its passage, high out-of-pocket spending remains a key challenge for many: in a poll conducted in 2016, 43 percent of Americans reported difficulty paying for coverage, and 27 percent reported delaying needed care due to cost.

In the U.S., stories of four- and five-digit hospital bills facing the uninsured and underinsured abound. It is well known that many Americans lack adequate health insurance coverage; prior to the passage of the Affordable Care Act in 2010, 18.2 percent of Americans were uninsured. Even following its passage, high out-of-pocket spending remains a key challenge for many: in a poll conducted in 2016, 43 percent of Americans reported difficulty paying for coverage, and 27 percent reported delaying needed care due to cost.

High out-of-pocket spending on health care is a serious concern for the least well off in the U.S., but what about those Americans that are fortunate enough to have a high-quality health insurance plan and a powerful national insurer to negotiate lower health care prices? With comprehensive coverage and insurer-negotiated rates, these patients would never be subject to such sky-high hospital bills …would they?

In research published in the journal JAMA Internal Medicine, I, along with colleagues from the University of Michigan, set out to examine this question. Using health insurance claims data from major U.S. insurers, we analysed out-of-pocket spending for 7.4 million inpatient hospitalisations among non-elderly adults enrolled in employer-sponsored and individual market health insurance plans from 2009 to 2013.

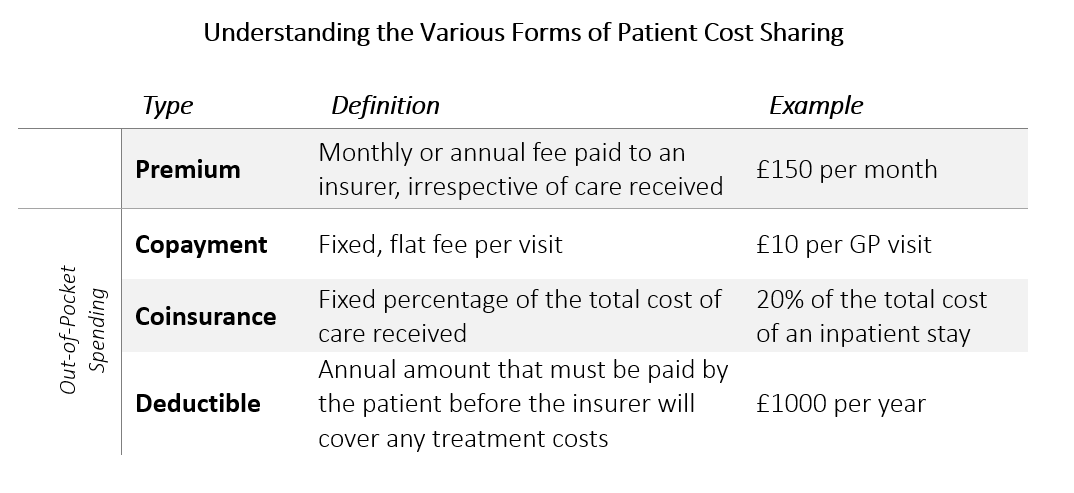

Out-of-pocket spending, which may include copayments, deductibles, and/or coinsurance, is the amount of money that patients are responsible for “cost sharing” with their insurer when they receive treatment. Originally devised as a way to reduce overuse of health care, high levels of out-of-pocket spending may impede access to necessary care and affect treatment decisions.

We found that over two-thirds of hospitalisations for insured adults required some form of out-of-pocket spending. After accounting for inflation and case-mix differences across years, our results showed that out-of-pocket spending for an inpatient hospitalisation grew by more than 37 percent over the study period, from a mean of $738 to $1,013 (approximately £556 to £763). This represents an annual growth rate of 6.5 percent. By comparison, health insurance premiums grew at an annual rate of 5.1 percent from 2009 to 2013. More broadly, this coincided with a significant slowdown in the growth of overall health care spending in the U.S., which rose at a rate of just 2.9 percent over this same time period.

Breaking this down further, we found that the amount applied to patients’ deductibles grew by 86 percent over the study period, and coinsurance grew by 33 percent. In contrast, fewer inpatient hospitalisations required a copayment over time. This suggests a trend toward fewer plans requiring copayments at the point of service, and more plans requiring higher coinsurance and payment towards a deductible after care is delivered.

These findings are particularly striking when you consider that most Americans are poorly informed about the different types of cost sharing associated with medical care. A 2013 survey of enrolees in employer-sponsored health insurance plans found that only 11 percent of respondents could correctly estimate the cost sharing associated with a hospital stay when provided with information regarding the cost of the admission and plan benefits, and only 14 percent of respondents were able to provide correct answers to a set of four multiple-choice questions relating to deductibles, copayments, coinsurance and out-of-pocket maximums.

In other words, not only is cost sharing for inpatient hospitalisations high and rising – even among insured individuals – but the complicated nature of cost sharing and health insurance benefit design means that many seemingly well-insured Americans may unknowingly face considerable financial risk when they are hospitalised.

The Affordable Care Act introduced cost sharing subsidies as well as annual out-of-pocket spending maximums (effectively capping the amount that patients have to pay out-of-pocket each year) to help shield patients from some of these high costs. However, at $7,350 (approx. £5,539) for individuals and $14,700 (approx. £11,078) for families in 2018, patients face a substantial financial burden before reaching these annual out-of-pocket maximums. In addition, these provisions only apply to those that obtain coverage through a marketplace plan, and thus do not necessarily apply to the many individuals that receive insurance benefits through an employer.

Clearly, high costs are a function of the U.S. system broadly speaking. However, high out-of-pocket spending isn’t just an issue facing the uninsured, it is a major issue for most Americans, even those with so-called “high quality” health insurance plans. Given that over 80 percent of commercial health insurance benefit packages now require coinsurance for inpatient hospitalizations in addition to meeting an annual deductible, high and rising cost sharing for inpatient hospitalisations is a critical, and oft overlooked, area for policy reform in the U.S.